حوّل رؤى الذكاء الاصطناعي إلى أفعال منسّقة

الرائج الآن

Categories

Aircraft Aftermarket: Market Size and Share Analysis

Aircraft Aftermarket: Market Size and Share Analysis

The global aircraft aftermarket is witnessing substantial growth, propelled by increasing air traffic, an aging fleet of both commercial and military aircraft, and a growing emphasis on operational efficiency, safety, and performance. Valued at $29 billion in 2023, the market is expected to expand from $30.16 billion in 2024 to $41.28 billion by 2032, representing a compound annual growth rate (CAGR) of 4% over the forecast period.

Growth Drivers and Market Segments

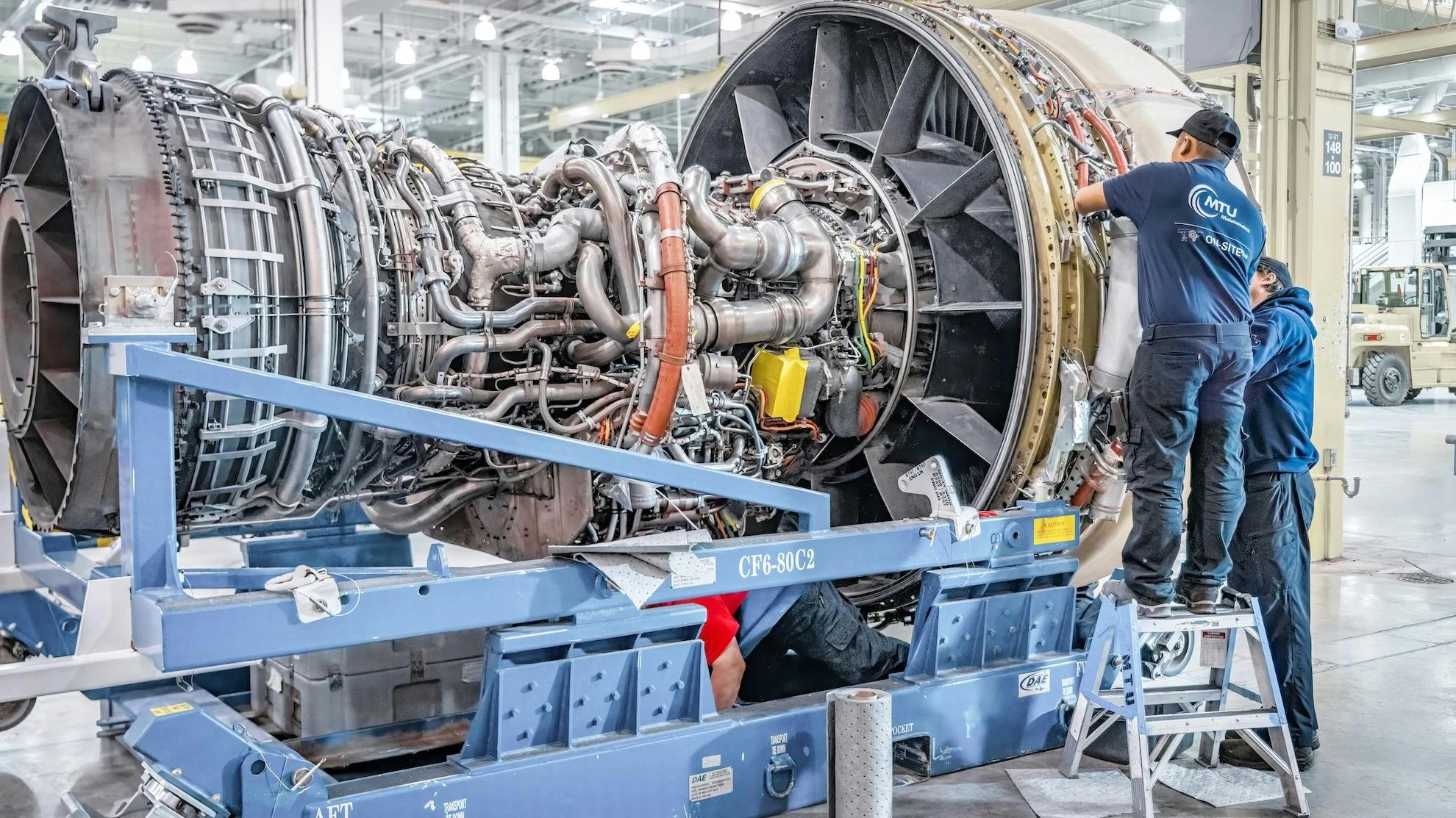

A key driver of this expansion is the Maintenance, Repair, and Overhaul (MRO) segment, which is projected to reach $90 billion in 2024 and rise to $155 billion by 2034. Airlines and operators are increasingly allocating resources toward high-quality MRO parts and services, as well as aircraft upgrades, to extend the lifecycle of their assets while managing maintenance expenditures effectively. This strategic investment reflects the sector’s focus on sustaining operational readiness and cost control.

Challenges Facing the Aftermarket

Despite promising growth prospects, the aircraft aftermarket confronts several significant challenges. Regulatory compliance remains a foremost concern, with stringent safety and certification standards elevating operational costs and potentially prolonging lead times for new aftermarket solutions. The highly regulated nature of the aviation industry demands that all aftermarket products and services adhere to comprehensive standards, adding layers of complexity for providers.

Market dynamics are further influenced by fluctuating fuel prices, global economic volatility, geopolitical tensions, and variations in airline profitability, all of which affect operational budgets and MRO spending patterns. Additionally, recent disruptions in supply chains and shortages of skilled labor have complicated the operational landscape, increasing costs and occasionally causing delays in service delivery.

Technological Innovations Transforming the Industry

Technological advancements, particularly the integration of Artificial Intelligence (AI) and the Internet of Things (IoT), are reshaping the aircraft aftermarket. These innovations are revolutionizing MRO activities by enabling predictive analytics and condition-based maintenance. IoT sensors embedded in aircraft components provide real-time data, facilitating early detection of potential failures and optimizing maintenance schedules. This transition from traditional scheduled maintenance to predictive approaches reduces unscheduled downtime, prolongs asset life, and enhances both safety and operational efficiency.

A notable example occurred in 2024 when a major airline collaborated with an aerospace technology firm to implement an AI-powered predictive maintenance platform. By analyzing engine sensor data, the system accurately forecasted component failures, allowing maintenance teams to preemptively order parts and schedule repairs during planned downtime. This initiative not only lowered costs but also minimized unexpected maintenance events, thereby maximizing aircraft availability.

Market Outlook and Competitive Landscape

The demand for smart maintenance solutions is anticipated to accelerate, with the aviation smart maintenance market projected to reach $12 billion by 2034. Similarly, the market for aircraft safety check automation is expected to grow from $1.2 billion in 2024 to $2.5 billion by 2034. In response to these trends, industry competitors are investing heavily in advanced technologies and adopting competitive pricing strategies to capture larger market shares.

While the aircraft aftermarket is positioned for significant growth, it must continue to navigate regulatory, technological, and operational challenges. The ongoing adoption of AI, IoT, and automation technologies is poised to play a critical role in enhancing efficiency and sustaining the sector’s expansion in the years ahead.

Qatar Airways and Industry Leaders Unveil New Aircraft and Innovations at Farnborough Airshow 2026

Kenya Airways Considers Boeing 777 Freighters and E2 Jets

Horizon Aircraft Selects BETA Systems for Cavorite X7 VTOL Jet

Malaysia Plans New Aviation Rules to Support Aerospace Growth, Says Loke

MTU Highlights CFM Partnership in Launch of Fort Worth Hub

IBS Group Launches Naviq Technology to Advance AI in Travel Industry

Rise in AI and SpaceX Fortunes Fuels Private Jet Demand

AJet to Add Five A321neos to Fleet

AeroDirect Expands CFM56 Engine Offerings

The Five Stages of Airport Intelligence: A Roadmap to 2040