Orchestrer les insights d’IA pour les transformer en actions

Tendances

Categories

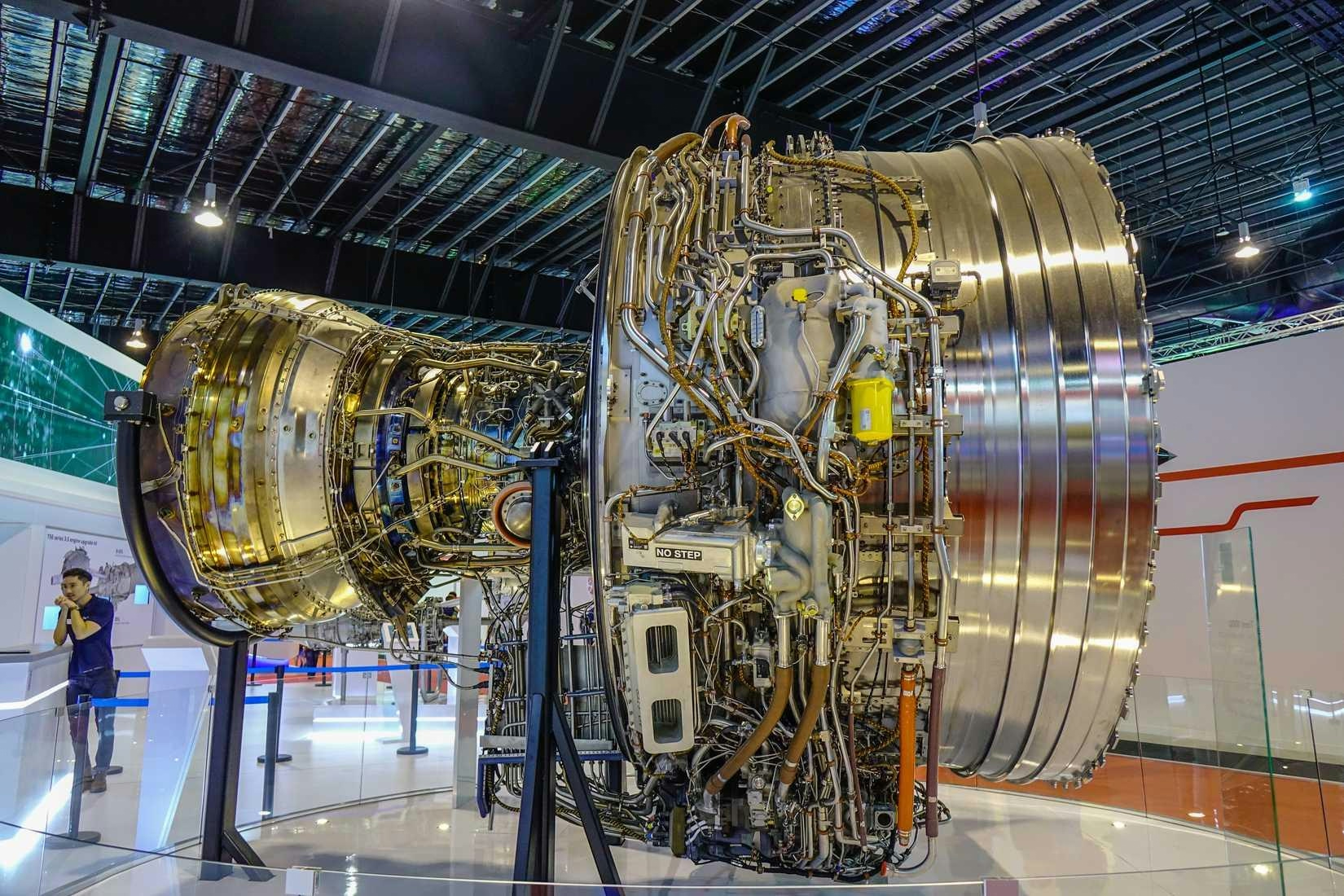

Boeing 787-9 Leads Widebody Activity in October

Boeing 787-9 Leads Widebody Activity in October

Boeing and Airbus maintain their dominance in the widebody aircraft market, with Boeing’s twin-aisle jets scheduled for 138,145 flights in October 2023, representing a modest 0.7% increase compared to the previous year, according to aviation analytics firm Cirium. More notably, the available seat miles (ASMs) on Boeing widebody flights have risen by 3.5%, suggesting that these aircraft are increasingly deployed on longer-haul routes.

Shift in Widebody Flight Activity

A significant development this year is the emergence of the Boeing 787-9 as the most active Boeing widebody aircraft. While the 777-300ER led widebody operations in October 2022 with 35,051 flights, its usage has declined by 2% to 34,367 flights this October. In contrast, the 787-9 has experienced a substantial increase, with 34,903 scheduled flights—a 10.8% rise year-on-year. These flights collectively offer over 10 million seats and nearly 36.8 billion ASMs, marking increases of 10.8% and 12.5%, respectively.

Boeing attributes the success of the 787 to its role in enabling more than 425 new nonstop routes worldwide, many of which were previously unserved. The Dreamliner fleet has transported over one billion passengers faster than any other widebody jet in history. Boeing highlights the aircraft’s advanced technology as a critical factor driving airline growth and enhancing the passenger experience.

Airline Operations and Market Dynamics

The growing prominence of the 787-9 is reflected in airline scheduling this October. Etihad Airways leads as the top operator, with 2,428 flights, offering 692,340 seats and over 2.4 billion ASMs. Its busiest 787-9 routes from Abu Dhabi are to Milan Malpensa and Phuket, each with 59 rotations. All Nippon Airways, the 787’s launch customer and last year’s leader, has fallen to second place with 2,175 flights, an 8.1% decrease. Its busiest route remains the domestic Tokyo–Fukuoka corridor, with 69 round trips. Qatar Airways ranks third, operating 1,994 787-9 flights—a 26.9% year-on-year increase—with Doha–Barcelona as its top route.

Further underscoring the 787-9’s momentum, WestJet recently placed an order for seven additional aircraft, effectively doubling its widebody fleet. Boeing is also engaged in advanced negotiations to sell 500 commercial jets to China, a strategic move aimed at regaining market share from Airbus amid intense competition.

Regional Recovery and Industry Outlook

Despite these gains, the Asia-Pacific region’s recovery remains uneven, with widebody activity still nearly 10% below pre-pandemic levels. Nevertheless, Boeing’s recent performance has been robust; in July 2025, the manufacturer delivered 10 widebody aircraft, surpassing Airbus’s eight deliveries for the month.

As airlines continue to rebuild and expand their long-haul networks, the Boeing 787-9 is emerging as a pivotal aircraft in driving growth and enhancing connectivity within the global widebody market.

Airbus and RVmagnetics Develop Sensing Mat for Aircraft Repair

Why Delta Air Lines Has Returned the Boeing 747 to Service

Aircraft Engine Troubleshooting at AirVenture

Iran Air Retires the Last Boeing 747SP, Ending an Era in Aviation

The Impact of Generative AI on Airline Distribution and Travel Retail

Unilode Introduces Fire Containment Cover Leasing for Airlines

Global Aviation to Double Capacity by 2050 Through AI and Software Without New Airports

Lithuania Reviews Future of Šiauliai International Airport

Four Air Taxi Models That Could Shape Future Travel

Rolls-Royce’s Trent 1000 XE Gains Ground on GEnx in Boeing 787 Market