AeroGenie — Votre copilote intelligent.

Tendances

Categories

IS&S Rebrands as Innovative Aerosystems to Focus on Aviation Technology

IS&S Rebrands as Innovative Aerosystems, Emphasizing Aviation Technology

EXTON, Pa. — Innovative Solutions & Support (NASDAQ: ISSC) has officially rebranded as Innovative Aerosystems, marking a strategic realignment of its brand identity and a sharpened focus on advanced aviation technology. The U.S.-based avionics company, recognized for its engineering and manufacturing solutions across commercial, business, and military aviation sectors, announced the change on Tuesday. The move underscores the firm’s commitment to integrating intelligent system designs with next-generation avionics.

Shahram Askarpour, President and CEO of Innovative Aerosystems, stated, “Innovation has always been the driving force behind everything we do. Our new name reflects the company’s expanded vision and future direction.” Despite the rebranding, the company assured customers that its core values and dedication to service remain intact, with existing product lines and support services continuing without interruption.

Financial Performance and Market Challenges

The rebranding coincides with a period of strong financial performance. Innovative Aerosystems reported a current ratio of 3.53 and nearly 73% revenue growth over the past year. Analysts at InvestingPro have rated the company’s financial health as “Good,” identifying 12 additional bullish indicators for the stock. However, the company’s Q3 2025 earnings report revealed a 105% year-over-year revenue increase, primarily driven by robust product sales, while earnings per share (EPS) remained flat relative to forecasts. This discrepancy, alongside concerns over shrinking gross margins and potential future revenue declines, has contributed to a sharp decline in the company’s stock price and raised investor concerns regarding long-term sustainability.

As Innovative Aerosystems embarks on this new phase, it confronts several challenges inherent to the competitive aviation technology market. The sector demands continuous innovation and adaptation amid industry-wide pressures related to growth and sustainability. Maintaining market relevance amid rapid technological advancements will be essential. Additionally, some stakeholders have expressed skepticism about whether the rebranding might affect existing client relationships or alter service offerings. Competitors are likely to respond by intensifying efforts to differentiate their services, leveraging established market positions, and accelerating the adoption of emerging technologies to counter Innovative Aerosystems’ renewed focus.

The company’s updated corporate website, now accessible at www.iascorp.com, reflects its refreshed branding. Innovative Aerosystems continues to serve both airframe manufacturers and aftermarket clients across fixed-wing and rotorcraft platforms, maintaining legacy product lines while advancing new navigation systems, flight deck displays, air data instrumentation, and other aviation technologies.

These developments illustrate both the opportunities and challenges facing Innovative Aerosystems as it seeks to strengthen its position in a rapidly evolving industry. For a comprehensive analysis of the company’s valuation and growth prospects, investors are directed to the full Pro Research Report available on InvestingPro, which provides expert insights and actionable intelligence on over 1,400 U.S. stocks.

Capital A Completes Sale of Aviation Business to AirAsia X

Four Gateway Towns to Lake Clark National Park

PRM Assist Secures €500,000 in Funding

Should Travelers Pay More for Human Support When Plans Go Wrong?

InterGlobe Aviation Shares Rise 4.3% Following January Portfolio Rebalancing

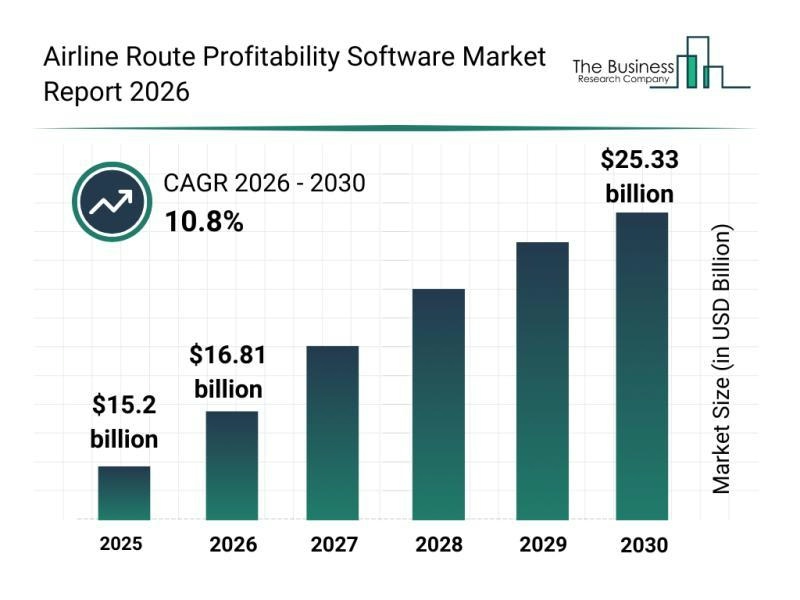

Key Market Segments Shaping Airline Route Profitability Software

Locatory.com Gains Traction Among Aviation MROs and Suppliers

JetBlue Flight Makes Emergency Landing Following Engine Failure

58 Pilots Graduate from Ethiopian University

The Engine Behind Boeing’s Latest Widebody Aircraft