Email più intelligenti, business più veloce. Tag automatici, analisi e risposte immediate a richieste, preventivi, ordini e altro.

Tendenze

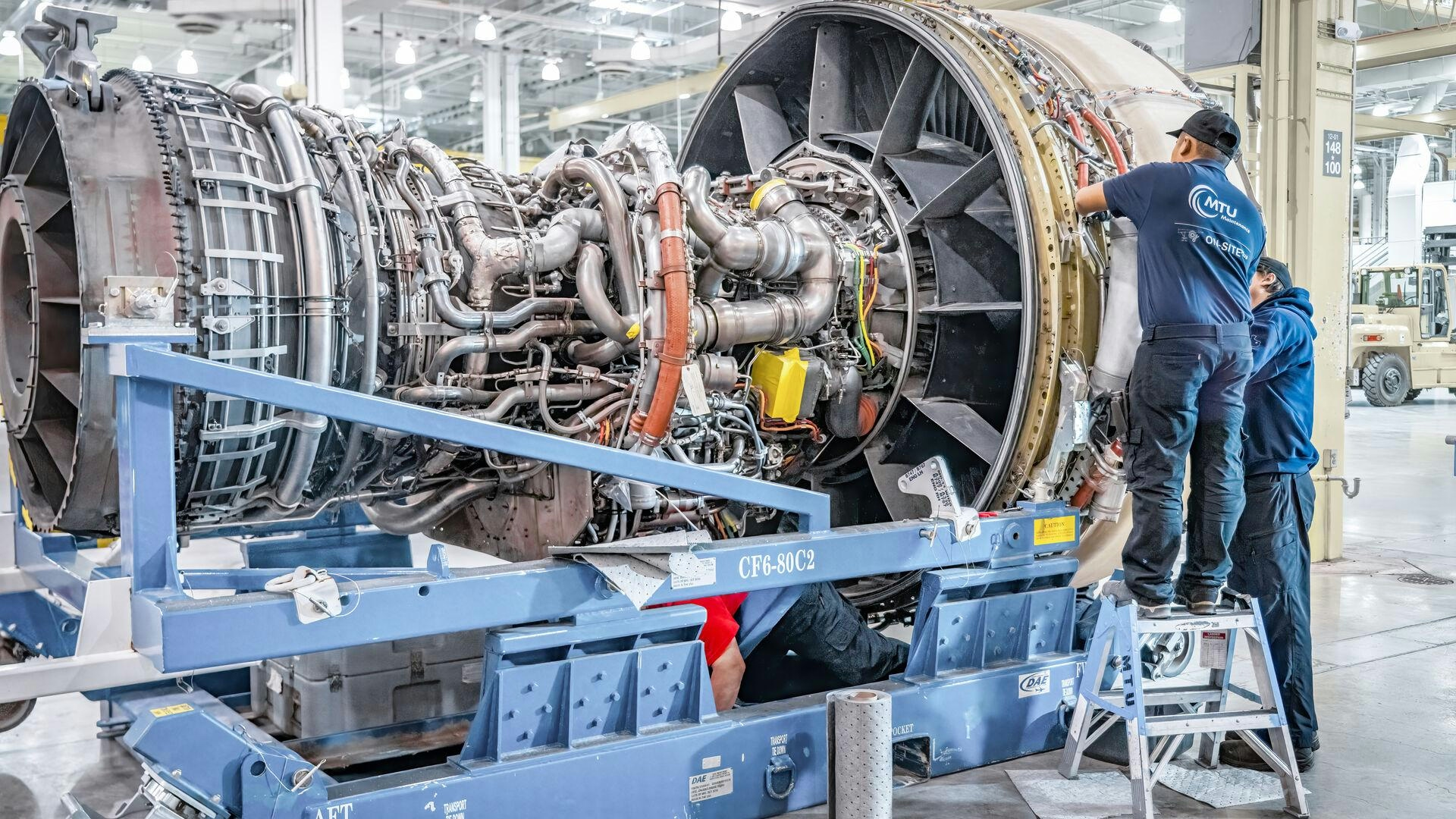

MTU Outlines Plan for MRO Expansion

MTU Outlines Plan for MRO Expansion

MTU Aero Engines has announced ambitious growth targets for its maintenance, repair, and overhaul (MRO) business, projecting that aftermarket revenues could double by 2030 and potentially triple by 2035. The company is transitioning its primary revenue focus from legacy IAE V2500 engine work to the expanding Pratt & Whitney PW1000G geared turbofan (GTF) fleet, supported by an expanding global overhaul network.

Strategic Growth and Revenue Projections

Chief Program Officer Michael Schreyogg revealed at a recent investor event that MTU aims to double its MRO revenue to approximately €10–11 billion ($11.8–13 billion) within the next five years. This growth is underpinned by continued investments in key platforms such as the CFM Leap and GE Aerospace GEnx engines, particularly through the company’s new facility in Fort Worth, Texas. Over the longer term, MTU anticipates maintenance revenues could reach between €15 and 16 billion. Last year, the company generated €5.5 billion in revenue, excluding joint ventures.

Central to MTU’s expansion strategy is the GTF program, where the company serves as a major risk-sharing and aftermarket partner. The GTF fleet is expected to achieve sales twice that of the V2500’s 7,800 units, signaling a significant shift in MTU’s revenue composition. This transition will reduce reliance on V2500 spare parts and foster a more balanced maintenance approach for the GTF engines, which is critical as manufacturers increasingly bear cost responsibilities. With over 80% of the GTF fleet operating under long-term service agreements, there is heightened emphasis on cost control for Pratt & Whitney and its partners. Schreyogg highlighted this shift, stating, “We now have started to really focus on MRO cost management. We look to repair parts instead of replacing parts.”

Market Dynamics and Technological Challenges

As the GTF program matures, MTU expects a reduction in the need for discounting to attract customers, with rising demand for MRO services across various platforms enhancing providers’ pricing power. Schreyogg noted, “There are no launch customer prices anymore out in the market. We have an opportunity to increase and improve our pricing given the current conditions.”

However, MTU’s expansion is not without challenges. The company is investing heavily in new technologies, including hydrogen fuel cell propulsion, which entails significant costs and technical complexities. While some investors are optimistic about the environmental benefits of such innovations, others remain cautious about their long-term economic viability. The competitive landscape is also evolving, with rivals pursuing similar propulsion technologies, potentially leading to a fragmented market. Furthermore, MTU’s growth ambitions may face regulatory hurdles and require substantial adaptations to existing aviation infrastructure.

Despite these obstacles, MTU remains steadfast in its commitment to expanding its MRO capabilities. The integration of the MTU Maintenance Dallas facility in Fort Worth into CFM’s official Leap overhaul network exemplifies this dedication. Schreyogg emphasized, “We are committed to invest in MRO, in maintenance, and in more capacity.”

As MTU navigates the complexities of a rapidly evolving aviation market and technological landscape, its focus on expanding MRO services and investing in next-generation propulsion technologies positions the company for sustained growth amid ongoing industry transformation.

Rising Costs Challenge Russia’s Push for Aviation Self-Sufficiency

Alaska Airlines Orders Additional Boeing 787s, Plans Dreamliner Base in Seattle

IndiGo and AI Express Boost Passenger Traffic at Hindon Airport with New Routes

Leading Aerospace Companies in Orlando

Embraer Reports Increase in Total Deliveries for Q2 2025

Report: AirAsia Nears Airbus Order

Rethinking Assurance Models in Aerospace

Estonia Sells Former Flag Carrier Nordica’s Fleet To U.S. Buyer

Houston Company Awarded $150 Million NASA Contract for Simulation Software