Orchestrer les insights d’IA pour les transformer en actions

Tendances

Categories

Rolls-Royce, Pratt & Whitney, and General Electric: Leaders in the Aircraft Engine Market

Rolls-Royce, Pratt & Whitney, and General Electric: Leaders in the Aircraft Engine Market

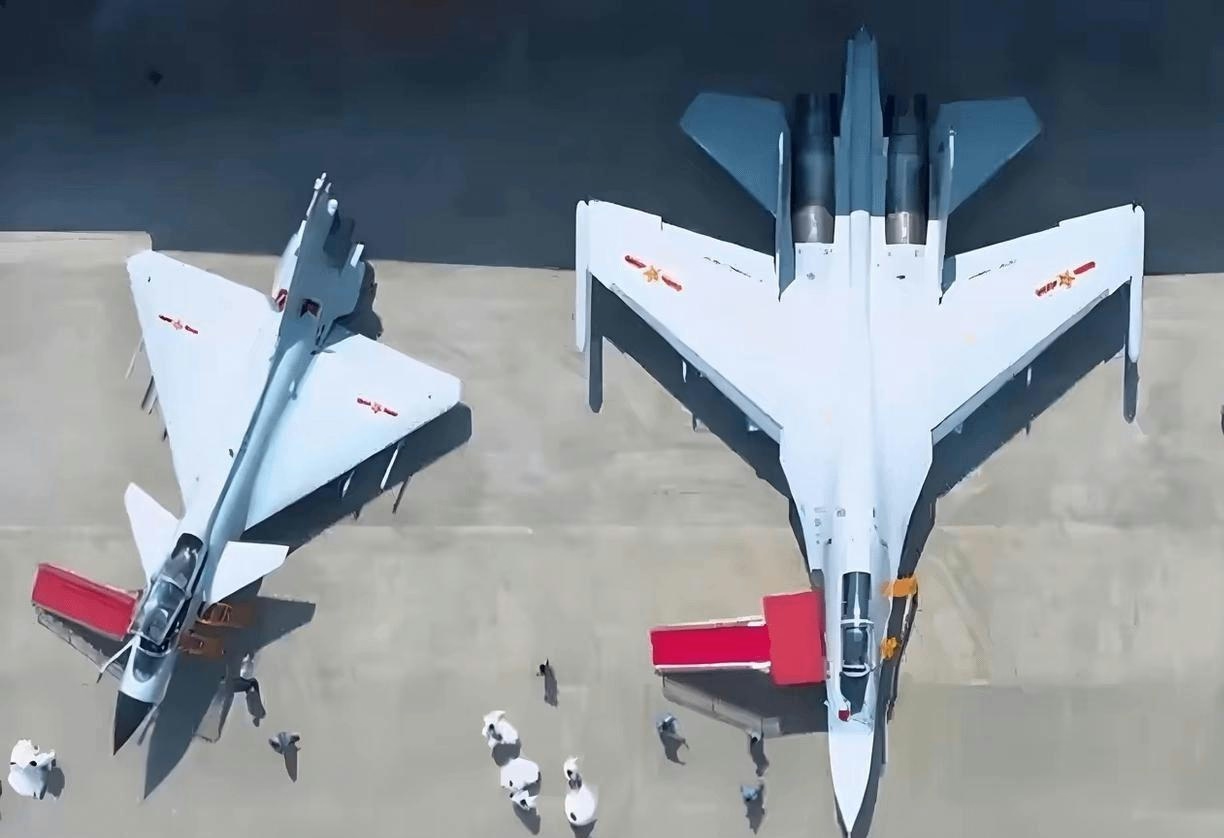

Aircraft engine manufacturers are fundamental to the aviation industry, providing the essential powerplants that enable commercial flight. Engines represent the most valuable component of an aircraft, accounting for up to half of the total value in modern jets. Beyond their monetary significance, engines are critical to operational efficiency and profitability. The global aircraft engine market is predominantly influenced by four major players: CFM International, General Electric (GE Aerospace), Pratt & Whitney, and Rolls-Royce. Each company holds a distinct leadership role within specific segments of the market.

Market Segmentation and Industry Growth

CFM International, a joint venture between GE and Safran, alongside Pratt & Whitney, dominates the single-aisle jet engine segment, powering widely used aircraft such as the Boeing 737 and Airbus A320 families. Rolls-Royce has carved out a strong position in the widebody market, particularly with its Trent engine series. GE Aerospace also commands a significant share of the widebody sector, powering half of the global widebody fleet, including the Boeing 747, 777, and 787 Dreamliner. Notably, GE is the exclusive engine supplier for the Boeing 777 and 747-8, while sharing the 787 platform with Rolls-Royce.

The aircraft engine industry is a multi-billion dollar sector, valued at over $81 billion in 2024 according to Global Market Insights. North America accounts for more than one-third of this market. Turbofan engines constitute over 70% of sales, reflecting their dominance in commercial aviation. The sector is experiencing robust growth, with a projected compound annual growth rate (CAGR) approaching 9%. By 2034, the market is expected to exceed $184 billion, with North America’s share alone surpassing the entire global market size of 2024.

While conventional engines currently dominate new orders, the industry is poised for a shift toward hybrid engine technologies over the next decade, particularly for regional aircraft. This transition highlights the sector’s increasing focus on innovation and sustainability.

Competitive Dynamics and Future Outlook

Competition within the aircraft engine market is intensified by the critical importance of aftermarket services. GE Aerospace recently raised its 2025 profit forecast, driven by strong demand in the aftermarket segment, which represents a vital revenue stream as engines typically retain value longer than airframes. Rolls-Royce is actively enhancing the durability of its Trent 1000 engine to maintain competitiveness against GE’s GEnx engine. The company’s stock has surged to record highs, supported by strong first-half financial results and a rebound in civil aerospace activity.

The aftermarket segment is becoming increasingly competitive, as demonstrated by the expansion of the Engine Assurance Program to include models from Rolls-Royce, GE Aerospace, and Pratt & Whitney Canada. This development underscores the growing significance of maintenance, repair, and overhaul (MRO) services within the overall market.

As the aircraft engine market continues to expand and evolve, Rolls-Royce, Pratt & Whitney, and General Electric remain at the forefront, navigating challenges and opportunities in technology, aftermarket services, and global demand. Their ongoing innovation and strategic positioning will continue to shape the future of aviation propulsion.

Qantas Prepares to Launch New 22-Hour Flight Route

Geopolitical Tensions and Supply Chain Disruptions Affecting Aviation Management in 2026

U.S. Customs and Border Protection Orders 10 Airbus H125 Helicopters for Border Security

Syrian President Plans to Order Eight Airbus Aircraft

China’s J-10 Fighter Used Russian Engines for Two Decades Before Domestic Powerplant Was Developed

Industries Affected by Global Political Tensions and Supply Chain Disruptions

UAE Certifies World's First Commercial Air Taxi Vertiport

Iran's Aviation Sector Reaches a Turning Point with Arrival of Former Saudia Boeing 777 Jets

Archer Aviation Shares Surge Amid Market Activity

FTAI and AEI Collaborate on 737-800 Freighter Conversion