Orquesta conocimientos de IA para convertirlos en acción

Tendencias

Categories

GE Aerospace Raises Full-Year Outlook Amid Aviation Recovery

GE Aerospace Raises Full-Year Outlook Amid Aviation Recovery

General Electric Co. has raised its full-year financial guidance and exceeded Wall Street’s profit expectations for the second quarter, driven by a strong rebound in the aviation sector. The company now projects adjusted earnings for 2025 to range between $5.60 and $5.80 per share, an increase from the previous upper estimate of $5.45.

Aviation Market Recovery and Operational Challenges

The improved forecast reflects a surge in global air travel demand as airlines ramp up operations. However, this recovery is tempered by ongoing delays in aircraft deliveries from major manufacturers Boeing and Airbus. These delays have compelled airlines to extend the service life of older jets, resulting in heightened demand for aftermarket maintenance services—a segment where GE Aerospace has experienced significant growth. Additionally, the company reported a substantial increase in jet engine deliveries, which has bolstered investor confidence and contributed to a positive market reaction.

Navigating Trade Tensions and Supply Chain Disruptions

Despite these positive developments, GE Aerospace continues to face a challenging global environment characterized by trade tensions and supply chain disruptions. The persistent global trade war has introduced uncertainties such as increased tariff costs and economic volatility. Competitors are actively implementing strategies to address supply constraints and mitigate the impact of tariffs, intensifying competition within the aerospace sector.

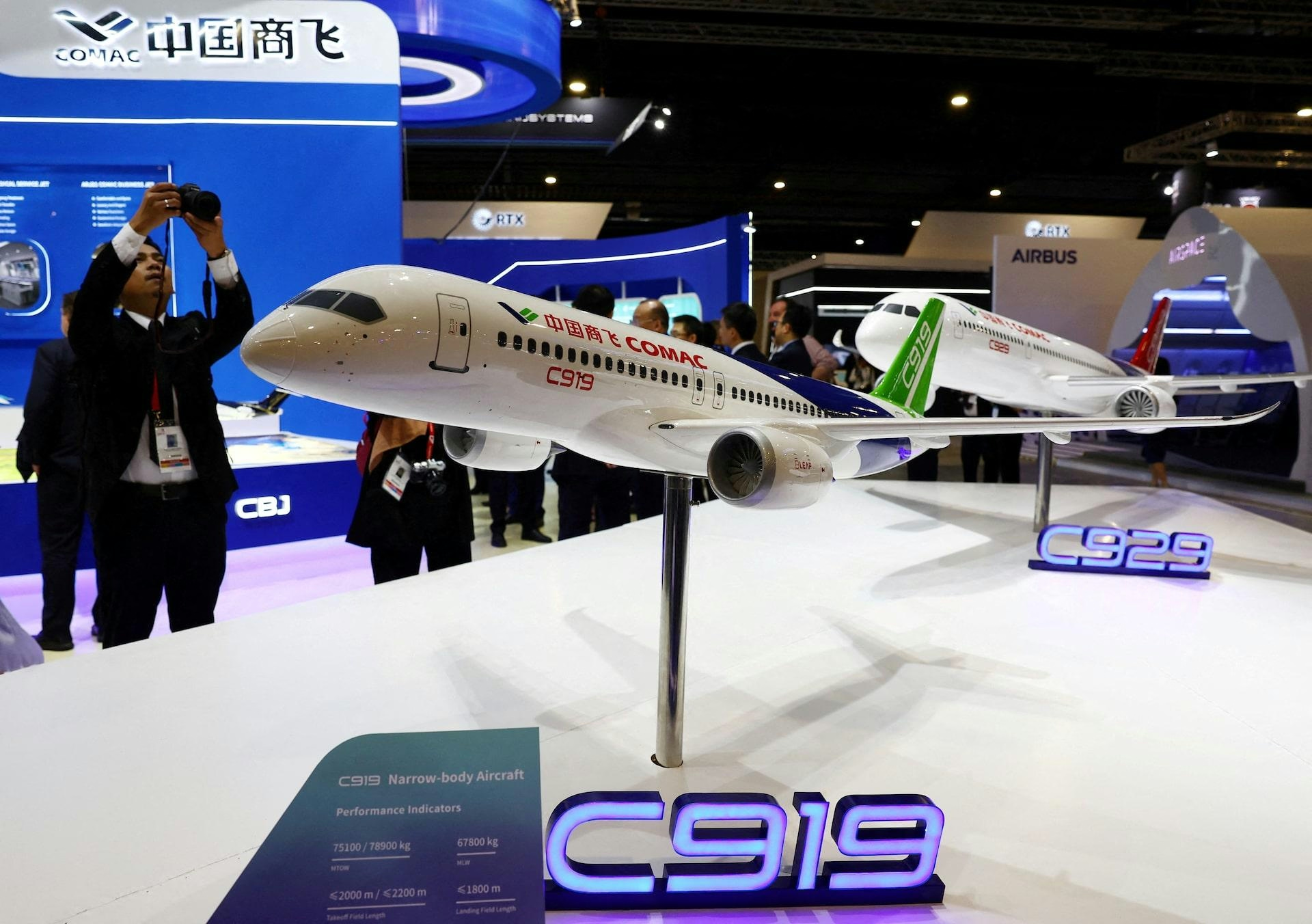

In a notable advancement, GE Aerospace has resumed jet engine shipments to China’s COMAC, indicating a potential easing of U.S.-China trade frictions. This development not only opens new avenues for business growth but may also alter competitive dynamics in the global aviation market, where access to China remains a critical factor for expansion.

While the recovery in aviation provides a strong tailwind, GE Aerospace remains cautious amid ongoing supply chain challenges and shifting trade policies. The company’s capacity to adapt to these headwinds will be essential as it strives to maintain momentum and achieve its revised financial targets.

Joby and Electra Executives Highlight Potential of Air Taxi Market

Boeing and Airbus Announce New Aircraft Orders at Farnborough Airshow

Honeywell Signs Major Avionics and APU Agreement with IndiGo for 2026

GE Aerospace Announces Advance in Hybrid-Electric Flight Technology

SMBC Aviation Capital Orders 100 Boeing 737 Max Aircraft

The Helicopter Company Orders Eight Additional Airbus H145s

RTX GTF Engine Reduces Fuel Consumption by 20% and Cuts Noise Footprint by 75%

Comac Returns to Farnborough as International Presence Expands

State Tax Service Reports One Aircraft Leasing Violation; Economic Security Bureau Investigates Five Airlines

Expeditors Expands Global Aircraft on Ground Services to Meet Growing Aviation Logistics Demand