Orchestrate AI insights into action

Trending

Categories

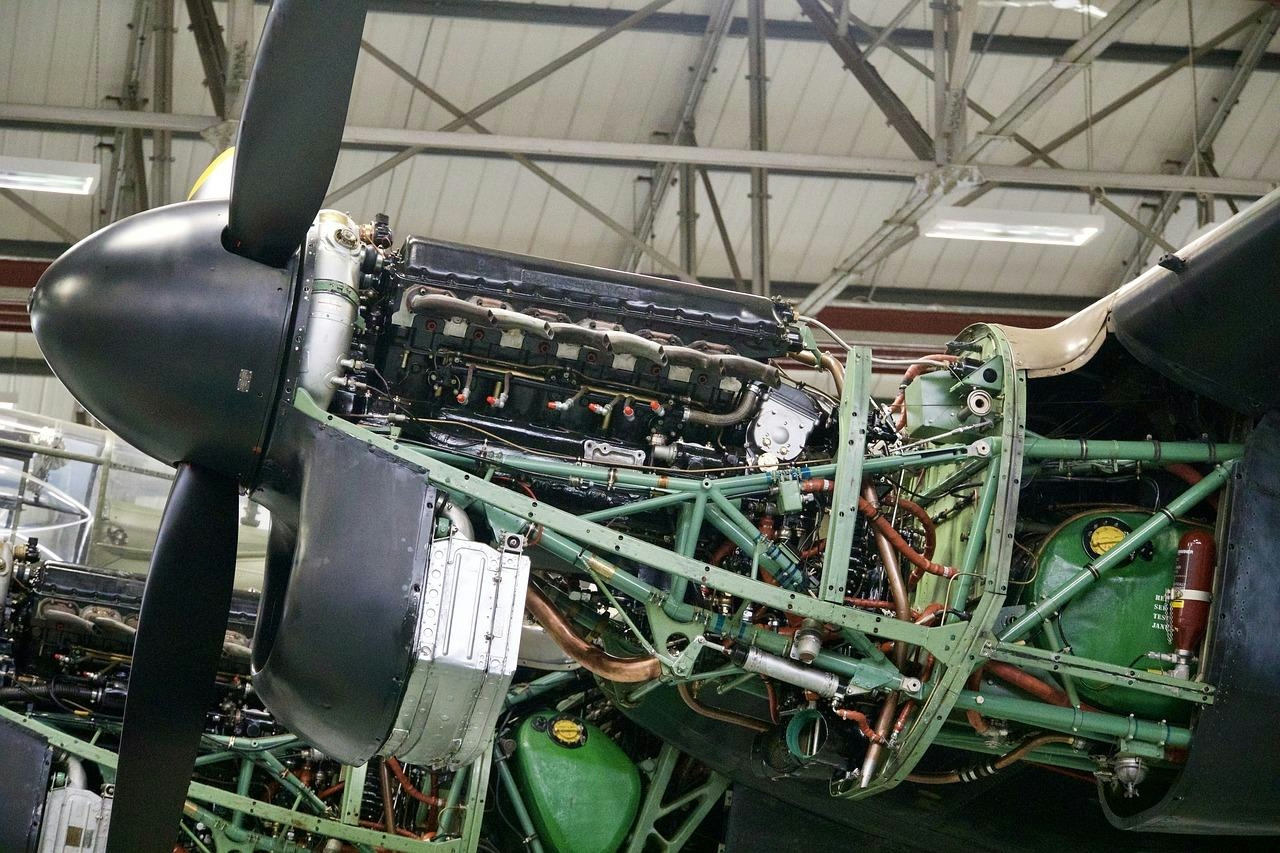

Adani Group to Enter Engine Maintenance and Aircraft Conversion Sectors

Adani Group Expands into Engine Maintenance and Aircraft Conversion

Adani Group is set to broaden its presence in the aviation sector by entering the engine maintenance and passenger-to-freighter aircraft conversion markets. This strategic expansion aims to enhance the conglomerate’s aviation services portfolio, complementing its existing investments in airport infrastructure and pilot training programs.

Strengthening Training and Maintenance Capabilities

In line with the anticipated growth of India’s aviation industry, Adani plans to significantly increase its simulator capacity nationwide. By bolstering its training infrastructure, the group seeks to meet the rising demand for skilled aviation professionals, thereby supporting the sector’s projected expansion. The move into engine maintenance and aircraft conversion represents a natural extension of these efforts, positioning Adani to offer a more comprehensive range of aviation services.

Competitive Landscape and Market Challenges

Adani’s entry into the maintenance, repair, and overhaul (MRO) space places it in direct competition with established players such as Ontic, PAG, and PrimeFlight. These incumbents have long-standing experience and well-established client relationships, creating a challenging environment for new entrants. Market responses to Adani’s expansion have been cautious, with some investors concerned about the substantial capital investment required to develop advanced maintenance facilities. The technical complexities and high operational costs associated with MRO activities may affect the group’s short-term financial results, even as it pursues long-term strategic benefits.

Industry Response and Future Prospects

Competitors are expected to respond assertively to Adani’s move into these sectors. Recent industry developments, including DAS Aviation’s acquisition of AQRD to enhance engineering and composites capabilities, illustrate a broader trend of established firms strengthening their service offerings to protect market share. Despite these challenges, Adani Group remains committed to its aviation growth strategy, leveraging India’s expanding air travel market and the increasing demand for integrated aviation services. The group’s investments across infrastructure, training, and now maintenance and conversion services underscore its ambition to become a significant player in the country’s evolving aviation landscape.

SITA: Software, Not Airports, Will Drive Aviation Growth

Frontier Airlines Revises Airbus A321neo Order Following Avolon Leasing Agreement

Airbus and RVmagnetics Develop Sensing Mat for Aircraft Repair

Why Delta Air Lines Has Returned the Boeing 747 to Service

Aircraft Engine Troubleshooting at AirVenture

Iran Air Retires the Last Boeing 747SP, Ending an Era in Aviation

The Impact of Generative AI on Airline Distribution and Travel Retail

Unilode Introduces Fire Containment Cover Leasing for Airlines

Global Aviation to Double Capacity by 2050 Through AI and Software Without New Airports

Lithuania Reviews Future of Šiauliai International Airport