Orchestrate AI insights into action

Trending

Categories

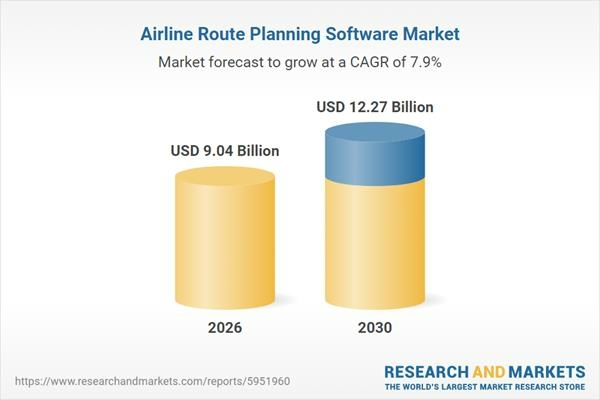

Global Airline Route Planning Software Market Forecasts Through 2035

Global Airline Route Planning Software Market Forecasts Through 2035

The global airline route planning software market is poised for significant growth over the coming decade. Valued at $8.36 billion in 2025, the market is projected to expand to $9.04 billion by 2026, representing a compound annual growth rate (CAGR) of 8.1%. By 2030, this figure is expected to reach $12.27 billion, driven by a sustained CAGR of 7.9%. This growth is underpinned by technological advancements in early flight scheduling, optimization tools, fuel efficiency analysis, and the integration of real-time weather and operational data, all of which are enhancing the precision and effectiveness of route planning.

Market Drivers and Emerging Trends

The increasing demand for fuel-efficient route planning and collaborative planning systems is shaping the market landscape. Mobile-based management interfaces are gaining traction, reflecting the industry's shift towards more flexible and accessible software solutions. The surge in global air travel further propels this demand. According to the International Air Transport Association, total air traffic rose by 26.2% year-over-year as of July 2023, with international traffic increasing by 29.6%. This rapid growth highlights the critical need for sophisticated software capable of optimizing flight routes, maximizing fleet efficiency, and improving cost-to-revenue ratios.

Leading companies in the sector are capitalizing on satellite-based flight tracking and advanced analytics to maintain competitive advantages. For instance, Cirium has developed tools that leverage satellite data to provide precise assessments of aircraft demand and network growth opportunities. In March 2023, Cirium introduced a new airline routes tool designed to enhance data-driven decision-making for route optimization. Strategic partnerships are also influencing the market’s evolution; notably, Riyadh Air’s collaboration with Sabre Corporation, announced in February 2024, aims to enhance operational efficiency through Sabre’s AirVision technology.

Regional Dynamics and Industry Challenges

The competitive landscape includes major players such as The Boeing Company, Airbus SE, Honeywell International, and Sabre. While North America currently dominates the market, rapid adoption is occurring in Asia-Pacific and Europe, driven by shifting trade relations and tariff impacts. The global trade environment, particularly the imposition of tariffs, is affecting costs related to essential hardware and cloud infrastructure. These pressures are fostering both challenges and opportunities, encouraging increased domestic software development and the expansion of regional data centers.

Despite the promising outlook, the market faces several challenges. Supply-chain disruptions, engine reliability concerns, and geopolitical uncertainties are increasingly influencing airline operations. In response, carriers are emphasizing flexibility in network planning. For example, Air Canada has adopted conservative fleet assumptions to mitigate associated risks. Competitors are refining route optimization algorithms to better navigate volatile operating conditions. Forecasts through 2035 indicate a continued focus on enhancing software capabilities to address these evolving challenges.

The comprehensive market report offers detailed analysis of market size, trends, and competitive dynamics across key regions including Asia-Pacific and Western Europe. It examines solutions related to fare management, scheduling, and revenue management, delivered through various platforms and pricing models. The report also provides revenue segmentation and market insights for countries such as Australia, Brazil, China, France, Germany, India, Japan, Russia, the United Kingdom, and the United States, encompassing the sale of related services and hardware.

Airline route planning software remains indispensable for efficient route management, resource optimization, and improved customer satisfaction. By accounting for factors such as fuel consumption, air traffic control, and weather conditions, these solutions are critical to the evolving demands of the global aviation industry. As the sector advances, the emphasis will remain on developing resilient, data-driven technologies capable of supporting a rapidly changing and increasingly complex operational environment.

Airbus Adapts A220 for Extended Transatlantic Flights

American, Delta, Southwest, and United Airlines Drive Major Changes in U.S. Aviation

Delta Ends Near-Free Upgrades to Increase Premium Revenue

Qatar Airways and Industry Leaders Unveil New Aircraft and Innovations at Farnborough Airshow 2026

Kenya Airways Considers Boeing 777 Freighters and E2 Jets

Horizon Aircraft Selects BETA Systems for Cavorite X7 VTOL Jet

Malaysia Plans New Aviation Rules to Support Aerospace Growth, Says Loke

Aviation Capital Group Obtains $1.48 Billion Unsecured Loan

Commercial Aircraft on Display at Farnborough 2026

MTU Highlights CFM Partnership in Launch of Fort Worth Hub